By Hirander Misra, Chairman, GMEX Group & MINDEX Holdings

With executives and experts in agreement over the immense market potential of blockchain solutions and tokenisation, Hirander Misra explains why investors should look at the Security Token Offering (STO) as an attractive fundraising instrument that hits the sweet spot between VC/PE on one hand and IPOs on the other.

A survey dubbed “Deep Shift Technology: Tipping Points and Societal Impact” of executives and experts by the World Economic Forum (WEF) in 2015 predicted that 10% of Global GDP would be stored on blockchain technology by 2027, which, based on 2018 GDP, amounts to around USD 8.5 trillion. When GDP growth is taken into account, the figure amounts to USD 24 trillion by 2027, according to analysis by institutional banking provider Finoa.

While the WEF survey looked at the impact of blockchain as a whole, it was recently estimated that the finance industry blockchain market may reach USD 462 billion by 2030, according to business information provider IHS Markit. The figure represents substantial growth when compared to the value of blockchain in the financial sector in 2017, at USD 1.9 billion. In March 2019, Cisco predicted a USD 10 billion annual blockchain market by 2021 in terms of project spend.

However, despite the bullish forecasts by industry and experts alike, blockchain technology still finds itself working hard to win investor trust, since some investors have burnt their fingers in fake Initial Coin Offering (ICO) projects. While this has resulted in the decline of ICOs, it has opened the door to a new type of token offering, the Security Token Offering (STO).

According to Bloomberg, the STO is “set to take centre stage in 2019”. As STOs gain more traction, investors can find more opportunities with fewer risks, as associated with ICOs, if they are structured correctly.

Will STOs disrupt the current intermediary model?

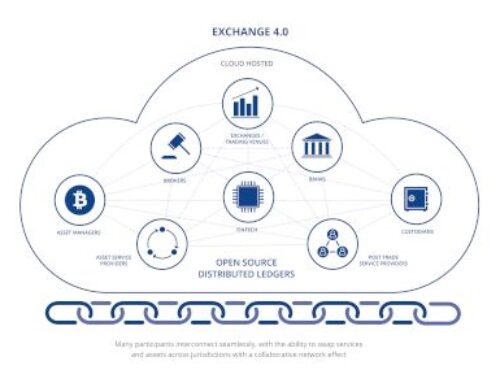

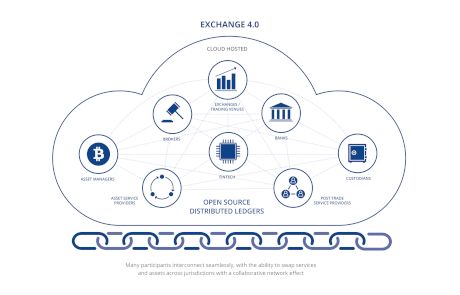

Indeed, it appears increasingly certain in view of their immense market potential that the current intermediary model will be disrupted by on-chain solutions and tokenisation – and will ultimately become more efficient. This will be applicable to banking, payments, exchanges and post-trade market infrastructure covering clearing and settlement, as well as wealth management, to name but a few sectors.

Whilst still in the early stages of market development for digital asset investments, one consequence is a reassignment of functions across the transaction value chain. For traditional securities, the institutional custodian function is typically provided by a third-party custodian, but this is not necessarily the case for digital assets where solutions can be provided by the digital exchange itself.

However, the custodian banks are looking to offer some form of digital custody services, with the majority focusing on tokenised assets that are backed by gold, property, securities and other real-world assets, as opposed to cryptocurrencies such as Bitcoin.

Is there a need for regulated digital exchanges and digital custodians?

I believe what the market really needs is access to asset tokens via regulated exchanges and stored in regulated digital custodians, delivering a level of security and oversight that is not currently available for digital assets.

Such a structure should offer proper legal nominee and escrow arrangements for the underlying asset to be tokenised, with valuations overseen by an established audit company, in the case of new issuance, or a credible custodian in terms of ongoing portfolio valuation and administration. This will help build trust for investors, whether they are high net worth or traditional buy side players like asset managers as well as ultimately retail investors.

How are traditional stock exchanges responding to STOs?

Some traditional stock exchange groups have announced plans to establish digital exchange projects focussed on security tokens and some, as an alternative expression to an STO, term the listing of products on their exchange as Initial Exchange Offerings (IEOs). With an IEO the exchange handles the whole process of token allocation and listing by acting as the counterparty as opposed to it just being a listing venue.

But this model still largely mirrors the market infrastructure framework and chain of intermediation that exists for traditional assets. These structures remain more expensive and contain a significant level of embedded operational inefficiency. They are also standalone much like the analogue phone of yesterday, whereas with blockchain the ability to interconnect different exchanges and asset custody pools of liquidity can become a reality, thus creating the equivalent of the smartphone of today.

This is expected to catalyse the ability of exchanges to more efficiently trade, clear and settle multiple types of digital assets across the globe.

How do STOs compare with traditional fundraising processes?

STOs hit that sweet spot between Private Equity (PE) / Venture Capital (VC), on the one hand, and Initial Public Offerings (IPOs), on the other hand, since they make the market more efficient as a result of there being fewer intermediaries. Through fractional ownership, you get a diversity of assets that can be opened up to a wider audience such as a single property divided into multiple tokens (units).

Without being tech experts, it can be harder for family office investors and retail investors to determine the difference between good and bad tokens; however, equity and value can be understood in the context when you can link the merits of STOs back to private equity. For example. STOs can also provide earlier liquidity to VC/ PE investors through fund tokenisation and as such should not be seen solely as an alternative to that mode of financing.

The table below cites some of my perceived advantages of an STO, especially in certain areas where VC/PE financing and IPOs may not allow investors to exploit the full spectrum of the investment opportunity:

Conclusion

Individuals and institutions need trusted solutions and the market is starting to respond to this with the launch of institutional grade digital exchanges and digital custodians. These will offer easier access to STOs and revolutionise the way that we do things by reinventing the current market infrastructure model.

Ultimately though, trust will continue to be key if we are to realise the 24-trillion-dollar opportunity represented by blockchain technology and to take this revolution to its full potential.

{kind=link}

{kind=link}