What will Britain’s role be as a financial innovation centre, post-Brexit? Our economy depends on it, yet over a year after our official exit from the EU on 31 January 2020, the answer is still not clear.

In 2018, GMEX Group and Greengage published a report and article highlighting “The ‘Digital Opportunity’ Of Brexit”. We looked at the economic opportunity for the UK to strike out on its own in shaping a unique approach to digital innovation after leaving Europe.

Our revised analysis, conducted 2 years later, suggests digital innovation could lead to an additional 300,000 high-value added jobs. The net result of focussing on digital innovation in the UK is estimated at 150,000 jobs and cumulative GDP growth of 5.7 percent over a 5 period. This would be more than enough to counter any potential losses due to Brexit. This estimate represents an uplift of 50,000 new jobs versus our 2018 analysis.

Britain’s existing achievements in Fintech means there is reason to feel confident in forecasting the UK’s capacity to realise the opportunities of a digital currency, digital ID, and DeFi (Decentralised Finance) as well.

UK Chancellor Rishi Sunak recently raised his own thoughts on how the UK can lead in digitisation and financial technology, announcing the launch of a new taskforce. He also confirmed that he will be taking forward many of the recommendations made in the recent Fintech Review and the Listing Review. In his recent speech, Sunak said: “if we can capture the extraordinary potential of technology, we’ll cement the UK’s position as the world’s pre-eminent financial centre”.

So what specific steps could the UK benefit from as part of a supportive industrial strategy? Stablecoins present a unique opportunity for the UK to participate in a reinvention of payment rails. China is already testing their national digital currency while the USA, with the world’s predominant reserve currency, is relatively behind. In addition to the efforts of private companies in this space, the UK could look at preparing a digital sterling to increase the attractiveness of GBP as a reserve currency (and reduce costs of debt borrowing).

The technology for Digital ID is already there and, with government support, it might be possible to build a consortium to make it happen. The potential for cost reduction in financial services for a consolidated KYC / AML process across industry participants is huge.

DeFi is nascent but if the UK were able to provide clear guidelines for bringing it into the regulatory perimeter (e.g. within guidance of FATF “Travel Rule”) and enforce KYC / AML there is also a considerable opportunity to steal a march. DeFi seems to be the killer app for digital beyond currency / payments efficiency and ID.

The economic argument for pursuing the above opportunities more than outweighs any potential downside from the economic impact of Brexit. For this to become a reality, the flagship initiative could be the UK’s “Britcoin” Central Bank Digital Currency (CBDC). This has the capacity to facilitate a more robust and transparent domestic and international commerce ecosystem – given the pound sterling’s role as an international reserve currency.

Delivering this will require a more forward-looking approach than exists currently. Strategy will need to be linked at all levels – government, regulatory bodies and industry – to drive forward collaborative changes. The UK needs clear leadership and advocates to deliver on Fintech’s promise, moving beyond consultation and into implementation.

Yet, if proposed policy changes can be implemented successfully, the UK can become not just a Fintech epicentre but can also propagate innovation and digital economic development across the globe. The question is can we afford not to seize this chance?

Hirander Misra, CEO of GMEX Group co-authored this article with Sean Kiernan, CEO of Greengage (previously DAG Global).

—

BACKGROUND INFORMATION AND SUPPORTING DATA

Nota Bene: Rationale for the revised report calculations for a post Brexit Digital UK:

Covid-19 has been a catalyst for change in the financial sector, especially in banking. The pandemic has forced many countries around the world to go on lockdown, resulting in customers unable to visit bank branches.

Real-time payments have revolutionised the retail funds transfer process by providing electronic cash to anyone in just a few minutes. Peer to peer money transfers has been around for a while and has witnessed high growth. Virtual currency, built on blockchain infrastructure, now offers better speed and efficiency of transaction.

The virus crisis is propagating the reassessment of bitcoin. Bitcoin is a growth asset that has performed strongly in an era of low returns from government bonds. PayPal said it would open its network to bitcoin and other cryptocurrencies. With digital adoption, more countries are moving towards cashless societies. Sweden, Norway, and Denmark are on course to becoming cashless societies and are adopting ‘no cash’ models.

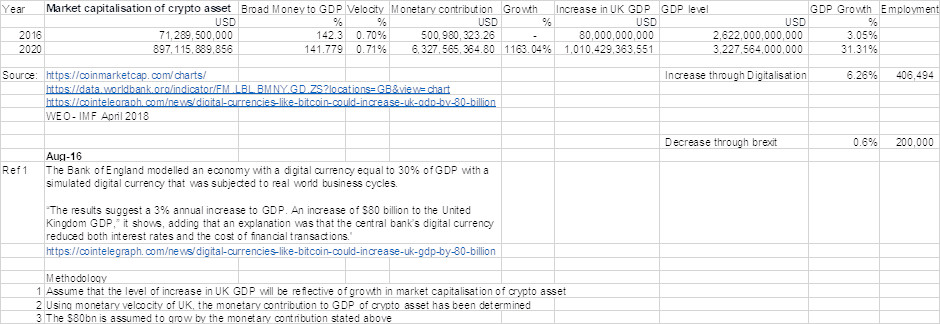

As per a research paper published by the Bank of England in 2016, the likely positive GDP effect of establishing a digital currency in the UK was 3%, that is an increase in $80b to UK GDP. Based on that, an assumption is made that this level of increase will be reflective of the growth of market capitalisation of crypto assets, having been adjusted for a lower adoption rate and using money velocity. The growth of monetary contribution from 2016 to 2020 is used to determine how much the $80b is likely to grow, which in turn contributes to our estimate of 5.7% of UK GDP growth cumulative over 5 years.

Our estimates are driven by the below supporting considerations:

- Based on the European Commission, for the EU on average, the exit of the UK from the European Union on Free Trade Agreement terms is estimated to generate an output loss of around 0.5% of GDP by the end of 2022, and some 2.25% point for the UK.

- The Office for Budget Responsibility predicted that Brexit would shrink the U.K. economy by 4% in the long run.

- IHS Markit estimated that the UK GDP would contract 1.4% in 2021 and 0.4% in 2022 before growth.

- A recent report on the UK in a Changing Europe suggests the cost will be 6.4% of GDP, with an annual reduction in growth of perhaps 0.5% as a result of the direct economic impact of Brexit.

- Based on research conducted by ABN AMRO, the base case is that 10 years after the referendum, UK GDP will be around 5% lower than it would have been had it voted to remain in the EU.

- S&P Global Ratings said in a report published 15 Dec 2020 that the U.K.’s GDP is forecast to expand by 4.6% in 2021, weaker growth than the 6.0% projected by S&P Global Ratings under an agreed-upon trade deal. The rating agency expects U.K. economic activity in 2023 to remain 1.4% short of levels that could have been attained with a core deal in place.

- A blog by Deloitte cited that most economic models assume that a more distant economic relationship with the EU will mean lower levels of inward investment and competition and reduced specialisation, and, therefore, lower long-term growth. Thirteen separate economic assessments of the impact on UK growth of operating under a free trade agreement showed an average reduction in the long-term level of GDP of 4.0%.

- Xavier Rolet, the former chief executive of the London Stock Exchange, predicted job losses of over 200,000.

- Research by Centre for Retail Research states that the high street shed 177,000 jobs in 2020 and predicts an even more devastating toll on retail jobs this year, with a further 200,000 expected to be lost.

- New analysis by PwC shows Blockchain technology has the potential to boost the UK’s GDP by £57bn ($72bn) over the next decade.

- The Treasury and Bank of England recently announced a joint task force to evaluate the creation of a central bank digital currency to future proof sterling against cryptocurrencies and improve the payments system. The macroeconomics of central bank issued digital currencies found that CBDC issuance of 30% of GDP, against government bonds, could permanently raise GDP by as much as 3% due to reductions in real interest rates, distortionary taxes, and monetary transaction costs.

- Dom Hallas, executive director at the Coalition for a Digital Economy (Coadec) in a review, said it was now important that people “follow through and actually implement” the ideas in the review. The sector’s direct contribution to the economy, it is estimated, will reach £13.7bn by 2030.

- According to the UK FinTech State of the Nation, there are +1600 FinTech firms in the UK and estimates suggest this will more than double by 2030. The UK’s FinTech adoption rate is 42% while the global average is 33%.

Appendix:

{kind=link}

{kind=link}

{kind=link}